Are hospice costs covered? A California family's guide

Are hospice costs covered? A California family’s guide

TL;DR:

- Most hospice costs in California are covered by Medicare, Medi-Cal, or private insurance.

- Proper documentation and timely forms are crucial to activating coverage and avoiding unexpected bills.

- Graceland Hospice Care assists families in navigating insurance paperwork to ensure seamless, stress-free care.

When a loved one receives a terminal diagnosis, the last thing your family should worry about is how to pay for compassionate care. Yet many California families hold back from pursuing hospice because they assume the costs will be overwhelming. The truth is that most hospice costs in California are covered when you know where to look. Medicare, Medi-Cal, and private insurance all play a role, and understanding these options can mean the difference between financial stress and peace of mind. This guide walks you through every major coverage source, how to qualify, and the practical steps that help your family secure the care your loved one deserves.

Table of Contents

- Understanding hospice costs and coverage in California

- Medicare and Medi-Cal: The backbone of hospice coverage

- Private insurance: What’s covered and what to watch for

- How to qualify: Physician certification, election forms, and critical steps

- Why understanding coverage nuances can save families thousands

- How Graceland Hospice Care makes coverage simple for families

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Most costs are covered | Major hospice expenses in California are usually paid by Medicare, Medi-Cal, or private insurance. |

| Eligibility depends on steps | A physician’s certification and a signed election form are required to qualify for coverage. |

| Room and board clarified | Medi-Cal now covers room and board in nursing facilities for eligible patients. |

| Private insurance varies | Check your plan for specific hospice benefits, as details like prior authorization and copays can differ. |

| Act quickly to avoid delays | Submitting all forms on time is crucial to prevent coverage gaps or extra costs. |

Understanding hospice costs and coverage in California

Hospice care is not a single service. It is a team-based approach to comfort and support during life’s final chapter, and it includes a wide range of services that, when billed individually, could add up quickly. Understanding what hospice covers and who pays for it is the first step toward feeling confident rather than anxious.

What hospice care typically includes:

- Physician and nursing visits at home or in a facility

- Medications related to the terminal diagnosis

- Medical equipment such as hospital beds, wheelchairs, and oxygen

- Personal care and aide services

- Social work support and counseling

- Chaplain or spiritual care services

- Bereavement support for family members

These services are bundled together under a single daily rate paid to the hospice provider, which is why coverage works differently than standard health insurance claims. You can learn more about how these services are organized in our hospice planning guide.

Over 95% of California hospice patients qualify for some form of coverage, whether through Medicare, Medi-Cal, or a private plan. That statistic often surprises families who assumed they would face large bills. The coverage landscape is broader than most people realize.

| Cost category | Typical coverage source |

|---|---|

| Nursing and physician visits | Medicare, Medi-Cal, private insurance |

| Medications (comfort-related) | Medicare, Medi-Cal, private insurance |

| Medical equipment | Medicare, Medi-Cal, private insurance |

| Inpatient crisis care | Medicare, Medi-Cal |

| Room and board (nursing facility) | Medi-Cal (for eligible patients) |

| Personal out-of-pocket items | Patient or family |

Medi-Cal covers hospice with no copays for eligible recipients, which means low-income families often pay nothing at all. Knowing which levels of hospice care apply to your loved one’s situation also helps you anticipate which services will be needed and fully covered. Even emergency care in hospice is addressed under structured coverage guidelines, so unexpected needs rarely result in surprise bills.

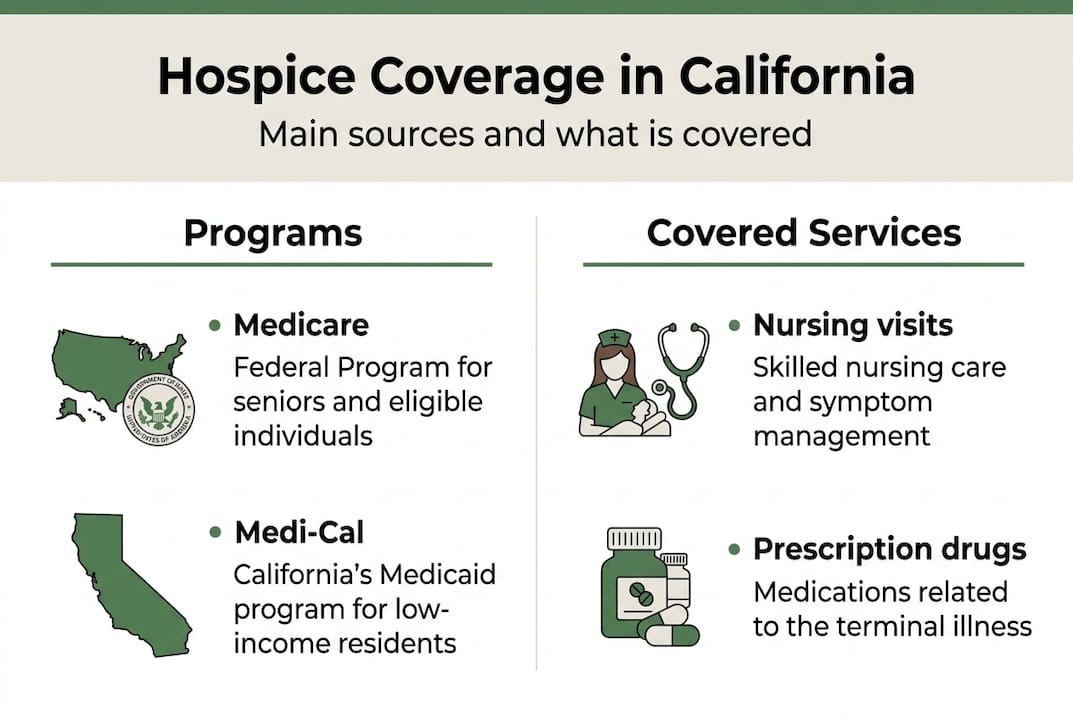

Medicare and Medi-Cal: The backbone of hospice coverage

For most California families, Medicare and Medi-Cal are the two programs that do the heaviest lifting when it comes to hospice costs. Understanding how each one works, and how they interact, can save you thousands of dollars and a great deal of confusion.

Medicare hospice benefit: Medicare covers hospice for any patient who is Medicare-eligible, has a terminal diagnosis with a life expectancy of six months or less if the illness follows its normal course, and formally elects hospice care by signing an election form. Once enrolled, Medicare pays the hospice agency a daily rate that covers all related services. There are no deductibles and no copays for most services.

Medi-Cal hospice benefit: California’s Medicaid program, Medi-Cal, mirrors Medicare for hospice coverage, and there are no copays for eligible individuals. Medi-Cal is available to California residents who meet income and asset requirements, and it often serves as a secondary payer for patients who have both Medicare and Medi-Cal.

One important 2025 update that carries into 2026: Medi-Cal pays room and board for dual-eligible patients in nursing facilities via pass-through payments. This change closed a significant gap that previously left some families with unexpected facility costs.

| Feature | Medicare | Medi-Cal |

|---|---|---|

| Eligibility | Age 65+ or disability | Income-based |

| Copays | None for hospice | None for hospice |

| Room and board (nursing) | Not covered | Covered for eligible |

| Duration | Renewable benefit periods | Ongoing while eligible |

| Prior authorization | Not required | Limited exceptions |

Completing end-of-life documentation in advance makes the enrollment process much smoother. Families who have paperwork in order before a crisis hits find that coverage begins quickly and without interruption.

Pro Tip: Do not wait until a health crisis forces the decision. Ask your physician about hospice eligibility early, and keep a folder with all insurance cards, identification, and income documents so that steps to start hospice can move forward without delay.

Private insurance: What’s covered and what to watch for

Not every family qualifies for Medicare or Medi-Cal. If your loved one has coverage through an employer, union, or individually purchased health plan, private insurance may be your primary option for hospice costs. The good news is that most private insurers operating in California do offer hospice benefits. The challenge is that the details vary widely from one plan to the next.

Private insurance often covers hospice but may require pre-authorization and can involve deductibles or out-of-pocket costs. Pre-authorization means the insurer needs to approve hospice services before they begin. Missing this step can result in denied claims, even if the care itself would have been covered.

Steps to check your private insurance coverage:

- Call the member services number on the back of the insurance card and ask specifically about hospice benefits.

- Request a written summary of benefits that includes hospice coverage details.

- Ask whether the hospice agency you are considering is in-network.

- Confirm whether pre-authorization is required and how long approval typically takes.

- Ask about deductibles, copays, and any annual or lifetime limits on hospice care.

- Get the name of the representative you spoke with and note the date and time of the call.

Common gaps in private coverage include a requirement to use a specific network of hospice providers, limits on inpatient respite days, and copays that apply to certain medications. Understanding these gaps ahead of time allows you to plan for any costs that may fall to your family.

Pro Tip: Always request written confirmation of coverage before starting hospice care. Verbal confirmations can be helpful, but written documentation protects you if a claim is disputed later.

“Reviewing your policy carefully and confirming coverage details in writing before hospice begins is one of the most important steps a family can take to avoid unexpected costs.” — Health Net California, 2026

Families often discover that choosing at-home hospice reduces out-of-pocket costs compared to facility-based care, particularly when private insurance has facility restrictions or daily rate limits.

How to qualify: Physician certification, election forms, and critical steps

Understanding who pays for hospice is important, but knowing how to activate that coverage is equally critical. Every coverage source, whether Medicare, Medi-Cal, or private insurance, requires a specific set of steps before payments begin. Skipping even one step can delay or disqualify your coverage.

Step-by-step guide to qualifying for hospice coverage:

- Talk to your physician. Ask directly whether your loved one’s condition qualifies for hospice. The physician must certify that the patient has a terminal illness with a life expectancy of six months or less if the disease runs its expected course.

- Choose a licensed hospice provider. In California, all hospice agencies must be licensed by the state. Confirm that your chosen provider is also certified to accept Medicare and Medi-Cal if applicable.

- Sign the hospice election form. This is the formal document that activates your hospice benefit. The patient or authorized representative must sign it, agreeing to focus care on comfort rather than curative treatment.

- Submit forms promptly. Certification and an election form are required to activate hospice coverage. For Medicare and Medi-Cal, submission within five days of the start of care ensures reimbursement is not delayed or reduced.

- Verify coverage with your insurer or case manager. Once forms are submitted, confirm receipt with your payer and ask for written acknowledgment.

One often-overlooked detail involves children. Under Medi-Cal, patients under the age of 21 can receive curative treatments at the same time as hospice care, a benefit that does not apply under standard Medicare rules. Physician certification requirements for children follow the same basic structure, but the option for concurrent care makes Medi-Cal particularly valuable for young patients and their families.

Knowing your hospice patient rights as a California resident also ensures that you can advocate effectively throughout this process. Families who understand what they are entitled to are far better positioned to ensure their loved one’s wishes are honored through every stage of care. Our guide on honoring hospice wishes walks through this in detail.

Why understanding coverage nuances can save families thousands

In our experience working with California families, the most common source of unexpected hospice costs is not a lack of coverage. It is a lack of awareness. Families who assume coverage is automatic or who delay paperwork often find themselves facing bills that should never have existed.

One area where this comes up repeatedly is managed care. Providers must submit election forms quickly, and managed care plans generally cannot require prior authorization except for inpatient care. Yet many families do not know this, and they wait for insurer approval before proceeding, creating unnecessary delays and, in some cases, gaps in coverage.

Another common mistake is assuming that Medi-Cal does not apply because the family believes they earn too much. Medi-Cal eligibility rules in California are more flexible than many people expect, particularly for individuals in long-term care settings. Asking the question costs nothing. Failing to ask can cost thousands.

The real insight here is that home hospice steps and coverage activation are not just administrative tasks. They are acts of advocacy for your loved one. Getting them right means your family can focus on presence, connection, and comfort rather than financial uncertainty.

How Graceland Hospice Care makes coverage simple for families

At Graceland Hospice Care, we understand that navigating Medicare, Medi-Cal, and private insurance paperwork is the last thing a grieving family wants to manage alone. That is why we do it with you. Our team helps families identify which coverage applies, complete all required forms on time, and avoid the common mistakes that delay benefits. We believe that compassionate care should never be out of reach due to confusion over paperwork. Explore our full range of hospice offerings and contact us today for a free consultation. We are here to make sure your loved one receives the dignified, supportive care they deserve, with as little financial stress as possible.

Frequently asked questions

Does Medi-Cal pay all hospice costs in California?

Yes, for eligible low-income patients, Medi-Cal covers hospice care and does not require copays, making it a complete coverage option for those who qualify.

Who pays for room and board in a nursing facility during hospice?

If your loved one has both Medicare and Medi-Cal, Medicare covers hospice services while Medi-Cal covers room and board in nursing facilities through direct payments to the facility.

What steps are needed to get hospice costs covered?

You need a physician’s certification of terminal illness and a signed hospice election form. Submitting these promptly within five days helps ensure there are no gaps in coverage.

Does private insurance cover hospice care in California?

Most private health insurers in California cover hospice, but coverage details and costs vary by plan, so always confirm your specific benefits and any pre-authorization requirements in writing.

Recommended

- Understanding Hospice Care Levels: A Guide for California Families | Graceland Hospice Care Blog

- End-of-Life Planning Guide: Hospice & Comfort Care at Home | Graceland Hospice Care Blog

- How hospice honors wishes in California: A complete guide | Graceland Hospice Care Blog

- Emergency care in hospice: a guide for California families | Graceland Hospice Care Blog