Medicare and Hospice Explained for Families in 2026

Medicare and Hospice Explained for Families in 2026

TL;DR:

- Medicare hospice provides comprehensive, comfort-focused care for terminal patients, allowing revocation and re-enrollment. Families should understand eligibility, coverage limits, and the importance of proactive communication with hospice providers. Early involvement and informed questions ensure access to the full support hospice and Medicare are designed to deliver.

When a loved one receives a terminal diagnosis, fear and confusion often arrive alongside the news. Understanding medicare and hospice explained clearly can make an enormous difference in how families respond. Far from signaling defeat, hospice care under Medicare represents a purposeful shift toward comfort, dignity, and whole-person support during life’s final chapter. This article walks you through eligibility, covered services, costs, and care levels so you can make informed, confident decisions for the people you love most.

Table of Contents

- Key takeaways

- Medicare and hospice explained: eligibility and enrollment

- What Medicare hospice coverage actually includes

- Understanding care levels and how Medicare pays

- Common misconceptions about costs and coverage

- Practical steps for families navigating hospice

- My perspective on what families truly need to know

- How Gracelandhc supports families through the Medicare hospice benefit

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Medicare Part A covers hospice | Patients must have Part A and a physician-certified prognosis of six months or less. |

| Comfort replaces curative care | Electing hospice means Medicare stops paying for curative treatment related to the terminal illness. |

| Broad services at minimal cost | Medicare covers nursing, medications, equipment, counseling, and respite care with little or no out-of-pocket cost. |

| Four care levels exist | Routine, continuous home, general inpatient, and respite care each serve different clinical needs. |

| You can revoke the benefit | Families can revoke the hospice election at any time and return to standard Medicare coverage. |

Medicare and hospice explained: eligibility and enrollment

The foundation of Medicare hospice coverage rests on three requirements. First, the patient must be enrolled in Medicare Part A. Second, the attending physician and the hospice physician must certify that the patient has a terminal illness with a prognosis of six months or less if the illness runs its natural course. Third, the patient must sign a hospice election statement choosing comfort-focused care.

Signing that election statement carries real weight. It is not simply paperwork. It is the formal declaration that the patient and family are shifting priorities from aggressive curative treatment to comfort and quality of life. At the same time, the patient waives Medicare payment for treatments aimed at curing the terminal illness, though Medicare still covers unrelated medical conditions.

Key facts about the enrollment process:

- Benefit periods: Two 90-day periods followed by unlimited 60-day periods, each requiring recertification.

- Face-to-face visits: A hospice physician or nurse practitioner must conduct a face-to-face visit before the third benefit period and each one after.

- Revocation: Patients may revoke hospice at any time to resume standard Medicare curative coverage. They can re-elect hospice later.

- Physician certification: Both the hospice medical director and the attending physician must agree on the terminal prognosis.

Pro Tip: Ask the hospice team to walk you through every line of the election statement before signing. Understanding exactly what Medicare will and will not cover from that point forward prevents billing surprises and helps you plan.

The process is more flexible than many families realize. Hospice is not a one-way door. The ability to revoke and re-elect gives families room to reassess without penalty, which is a detail that offers meaningful reassurance during an already stressful time.

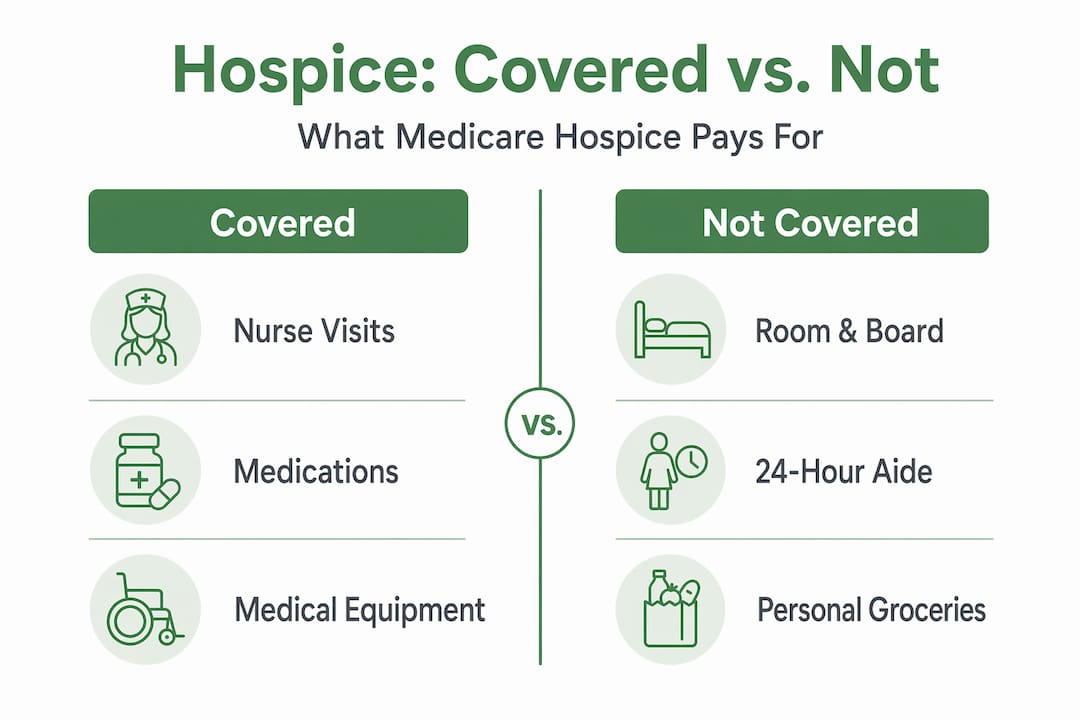

What Medicare hospice coverage actually includes

One of the most common surprises families encounter is just how broad Medicare’s hospice care benefits are. This is not a stripped-down benefit. It is one of the most comprehensive packages Medicare offers.

Covered services include:

- Skilled nursing visits on a schedule determined by the care plan, available 24 hours a day, seven days a week for urgent needs.

- Physician and advanced practice nurse services for symptom management and care plan oversight.

- Home health aide and homemaker services to assist with personal care and daily activities.

- Medical social work to help families manage emotional, practical, and financial challenges.

- Physical, occupational, and speech therapy when needed for comfort rather than rehabilitation.

- Medications for pain control and symptom management related to the terminal illness.

- Medical equipment and supplies such as hospital beds, wheelchairs, and wound care materials.

- Spiritual and dietary counseling addressing the whole person, not just the body.

- Short-term inpatient care for symptom crises that cannot be managed at home.

- Respite care for up to five consecutive days in a facility, giving family caregivers a needed break.

- Bereavement counseling for the family, available for at least 13 months after the patient’s passing.

| Service category | Covered by Medicare hospice | Patient cost |

|---|---|---|

| Nursing and physician visits | Yes | $0 |

| Pain management medications | Yes (terminal illness related) | Up to 5% coinsurance, capped per prescription |

| Medical equipment and supplies | Yes | $0 |

| Inpatient respite care | Yes (up to 5 days) | 5% coinsurance, capped at inpatient deductible |

| Bereavement counseling | Yes | $0 |

| Room and board in a facility | No | Paid by patient or family |

This level of support extends well beyond what traditional home health care typically provides. For families managing pain and symptom control at home, having a dedicated team available around the clock changes everything about the caregiving experience.

Understanding care levels and how Medicare pays

Medicare pays hospices a daily rate per enrolled day regardless of how many services are provided on a given day. That fixed payment model is worth understanding because it shapes how hospice organizations think about care.

The four levels of care Medicare covers are:

| Care level | Setting | When it applies |

|---|---|---|

| Routine home care | Patient’s home or facility | Day-to-day care without a medical crisis |

| Continuous home care | Patient’s home | Medical crisis requiring 8 to 24 hours of nursing |

| General inpatient care | Hospital or inpatient facility | Symptom crisis that cannot be managed at home |

| Inpatient respite care | Medicare-approved facility | Short-term caregiver relief, up to 5 days |

Because Medicare pays a daily flat rate, the hospice’s financial incentive aligns with doing more, not less. A well-run hospice monitors symptoms proactively and adjusts the care plan regularly rather than waiting for a crisis to develop. That is how proactive symptom management under Medicare’s payment model genuinely serves patients. CMS has also proposed a 2.4% payment rate increase for FY 2027, reflecting ongoing investment in hospice quality.

Pro Tip: When evaluating a hospice provider, ask how often the interdisciplinary team reviews your loved one’s care plan. Monthly reviews are standard. Weekly reviews for complex cases signal a provider that takes the daily payment model seriously.

Common misconceptions about costs and coverage

Families often arrive at hospice with assumptions that do not match reality. Clearing those up early prevents significant stress.

Hospice does not cover room and board. If a patient lives in a nursing home or assisted living facility, they still pay the facility’s room and board costs. Medicare hospice covers the clinical care delivered there, not the housing. This is one of the most frequently misunderstood aspects of hospice insurance coverage.

Electing hospice means waiving curative Medicare coverage for the terminal illness. The hospice election statement addendum now requires hospices to clearly explain which items and services are not covered under the benefit. This rule exists precisely because families were being caught off guard. Read it carefully.

Other points families frequently misunderstand:

- Coinsurance on medications is capped. During routine or continuous home care, patients may owe up to 5% coinsurance on palliative drugs, but that amount is capped per prescription. It is not unlimited exposure.

- Unrelated conditions are still covered by Medicare. If a hospice patient with cancer breaks an arm, standard Medicare covers the fracture treatment. Only curative care related to the terminal diagnosis is waived.

- New hospice provider enrollments are currently paused. CMS imposed a six-month moratorium on new hospice enrollments starting May 2026 to address fraud concerns. Patients already enrolled with existing providers are completely unaffected.

“Families should ask one simple question about every service: Is this related to the terminal illness? The answer tells you whether it falls under hospice coverage or remains with standard Medicare.” — Federal Register, Hospice Election Guidance

Understanding these boundaries is not about limiting care. It is about knowing where to look for support and how to ask the right questions without hesitation.

Practical steps for families navigating hospice

Knowing the rules is only half the work. Applying them during an emotionally charged time is the other half. These steps help families stay grounded and prepared.

- Request a copy of the plan of care. The individualized care plan is developed by the hospice interdisciplinary team and reviewed regularly. You have the right to see it, discuss it, and ask questions about every item on it.

- Ask about 24/7 access. Confirm the hospice provides on-call nursing and medical support at all hours. A provider that cannot offer this falls short of Medicare requirements.

- Clarify the election addendum. Before signing, walk through the addendum that lists non-covered services. This document, required under recent federal guidance, protects your family from unexpected bills.

- Know how to revoke. If you feel the patient’s condition has stabilized or you want to pursue curative treatment again, notify the hospice in writing. Medicare resumes standard coverage immediately.

- Engage the full team. Social workers, chaplains, and counselors are not optional extras. They are part of what makes hospice work. Families who engage the whole team consistently report better experiences and less caregiver burnout. Explore a practical at-home hospice care guide for additional support strategies.

Pro Tip: Keep a written log of all conversations with the hospice team, including dates, names, and what was discussed. If questions about billing or care decisions arise later, this record is invaluable.

Families who understand Medicare hospice guidelines and ask informed questions get more from the benefit. Advocacy and compassionate care work best together.

My perspective on what families truly need to know

I have spent years working alongside families who arrive at hospice feeling like they failed somewhere. They wonder if choosing comfort care means they gave up on their loved one. That feeling is understandable, and it is also wrong.

What I have seen, again and again, is that the families who thrive through this process are the ones who stop equating care with cure. The shift to palliative care is not a retreat. It is a decision to spend the time that remains focused on comfort, connection, and dignity rather than hospitalizations and procedures that may offer little benefit.

The billing and eligibility rules matter, and this article covers them carefully. But what I want families to carry with them is this: Medicare built hospice to be generous because lawmakers understood that end-of-life care requires more than medicine. It requires presence. The interdisciplinary team model reflects that understanding.

My honest advice is to get involved early. Too many families wait until the final days to elect hospice, missing weeks or months of support they were fully entitled to. If a physician has mentioned that a prognosis may be six months or less, it is not too soon to call a hospice and ask questions. Knowledge here is not morbid. It is a gift you give your family.

— Sam

How Gracelandhc supports families through the Medicare hospice benefit

Knowing your rights under Medicare is a starting point. Having an experienced, compassionate team beside you is what turns that knowledge into real relief.

Gracelandhc specializes in guiding families through every aspect of the Medicare hospice enrollment process, from verifying eligibility to explaining the election statement in plain language. The team at Graceland Hospice takes time to answer your questions, coordinate with attending physicians, and create a care plan that reflects your loved one’s specific needs and wishes.

If you are ready to learn how compassionate hospice care can support your family, Gracelandhc offers a free consultation to help you understand your options without pressure. Reach out today and let a dedicated team walk you through every step.

FAQ

Who pays for hospice care under Medicare?

Medicare Part A pays the hospice provider directly through a daily rate covering all covered services. Patients typically pay little to nothing out of pocket, with minor coinsurance for certain medications and respite care.

What are the hospice eligibility requirements for Medicare?

A patient must have Medicare Part A, receive physician certification of a terminal illness with a six-month or less prognosis, and sign a hospice election statement choosing comfort-focused care over curative treatment.

Does electing hospice mean giving up all Medicare coverage?

No. Electing hospice waives Medicare payment only for curative treatment of the terminal illness. Medicare continues to cover care for unrelated medical conditions through standard benefits.

Can a patient leave hospice and return to regular Medicare?

Yes. A patient can revoke the hospice benefit at any time in writing, immediately resuming standard Medicare coverage, and may re-elect the hospice benefit again later if needed.

What does Medicare hospice not cover?

Medicare hospice does not cover room and board in nursing homes or assisted living facilities, nor does it cover treatments aimed at curing the terminal condition. Unrelated medical conditions remain covered by standard Medicare.

Recommended

- Hospice Coverage in California: What Families Need to Know

- Why Hospice at Home Matters for Families | Graceland Hospice Care Blog

- Are hospice costs covered? A California family’s guide | Graceland Hospice Care Blog

- Understanding Hospice Care Levels: A Guide for California Families | Graceland Hospice Care Blog